In my new book, The 4 Actions A Small Business Owner Can Take To Lower Their Group Health Insurance Premium Next Month, I explain why business owners overpay for their group health insurance. It’s because many times they don’t purchase the most efficient plan available. To some business owners, the monthly premium is viewed as another necessary cost associated with operating their business and once their health insurance plan is in place, it is rarely analyzed and audited like other expenses. There is an emotional element that can become ingrained in a health plan and switching plans can be seen as an upheaval of sorts. But what if you could lower that expense? What if you could reduce your health care costs without sacrificing benefits, coverage and doctor networks?

If your total monthly group health premium is $6,000, a 24% cost savings would amount to a potential boost to your profits of over $17,000 per year.

What if that reduction could be as much as 24%? If your total monthly group health premium is $6,000, a 24% cost savings would amount to a potential boost to your profits of over $17,000 per year. Would that be worth taking a look at your options?

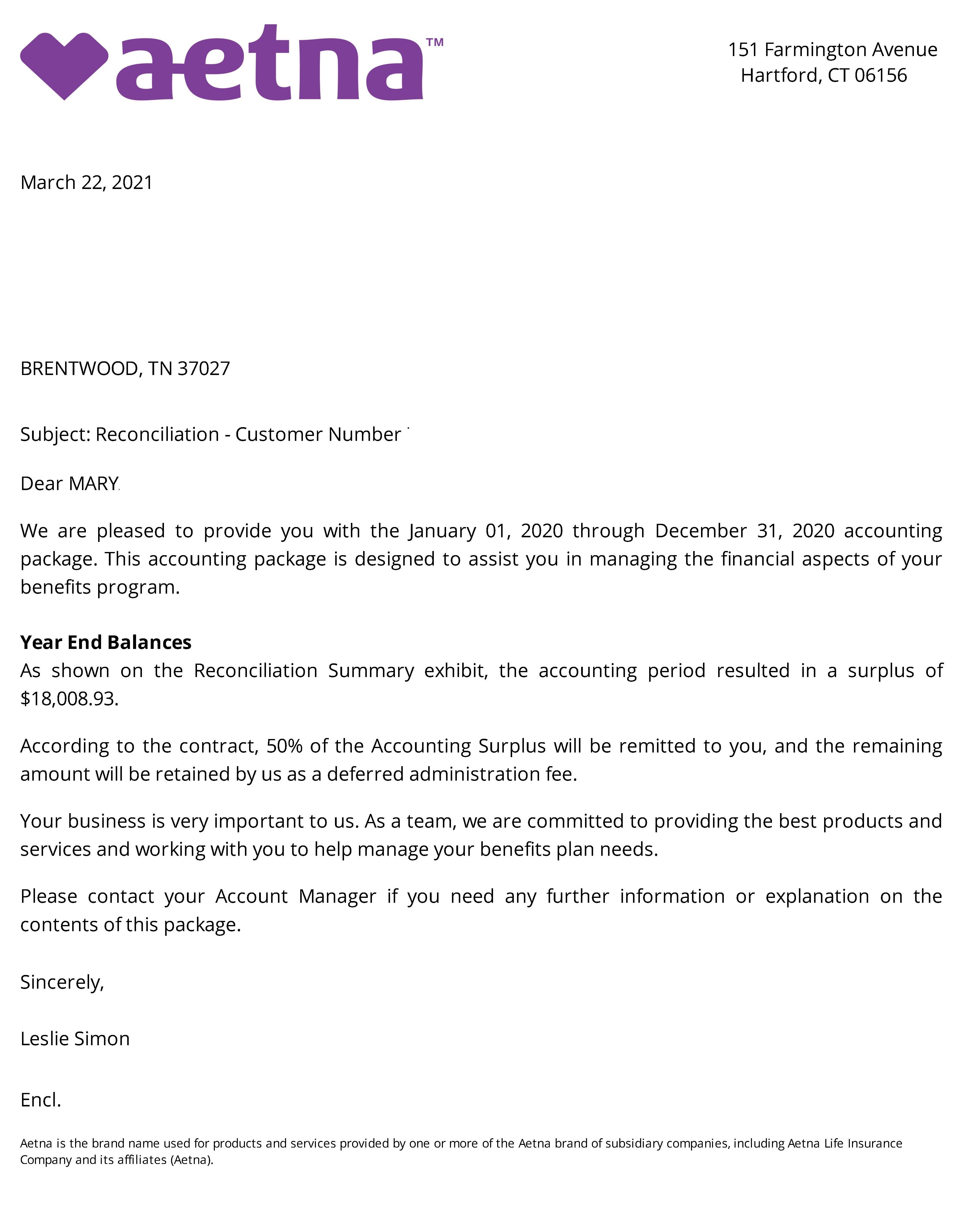

If that’s not enough to motivate you, what if at the end of the year, if your group was relatively healthy and had lower claims than anticipated, your group was entitled to a refund of some of your premiums? This is an email I received from one of my groups last year:

Hi, Rick. We received a letter from Aetna to let us know that our account created a surplus of around $12,000 for the last plan year. We will receive half of the amount. We are pleased with this result and want to thank you for setting us up in this type of plan.

Right now, all you have to do is take a few minutes to complete our census form. Once we have this information, we will analyze how much more efficient we can make your group health plan. We will do this analysis for no upfront cost or obligation.